阿联酋经济势头依然强劲,国内生产总值(GDP)持续增长,非石油部门不断扩大。通胀压力有所缓解,但租金水平依然居高不下,这继续制约着家庭消费能力。

在快速消费品领域,我们的2025年数据显示,随着每位消费者的有机消费量有所放缓,品类增长主要由人口增长驱动。尽管快速消费品的总销量有所上升,但这并非源于消费者购买量的增加,而是反映了更多家庭进入市场。

消费模式正在发生变化

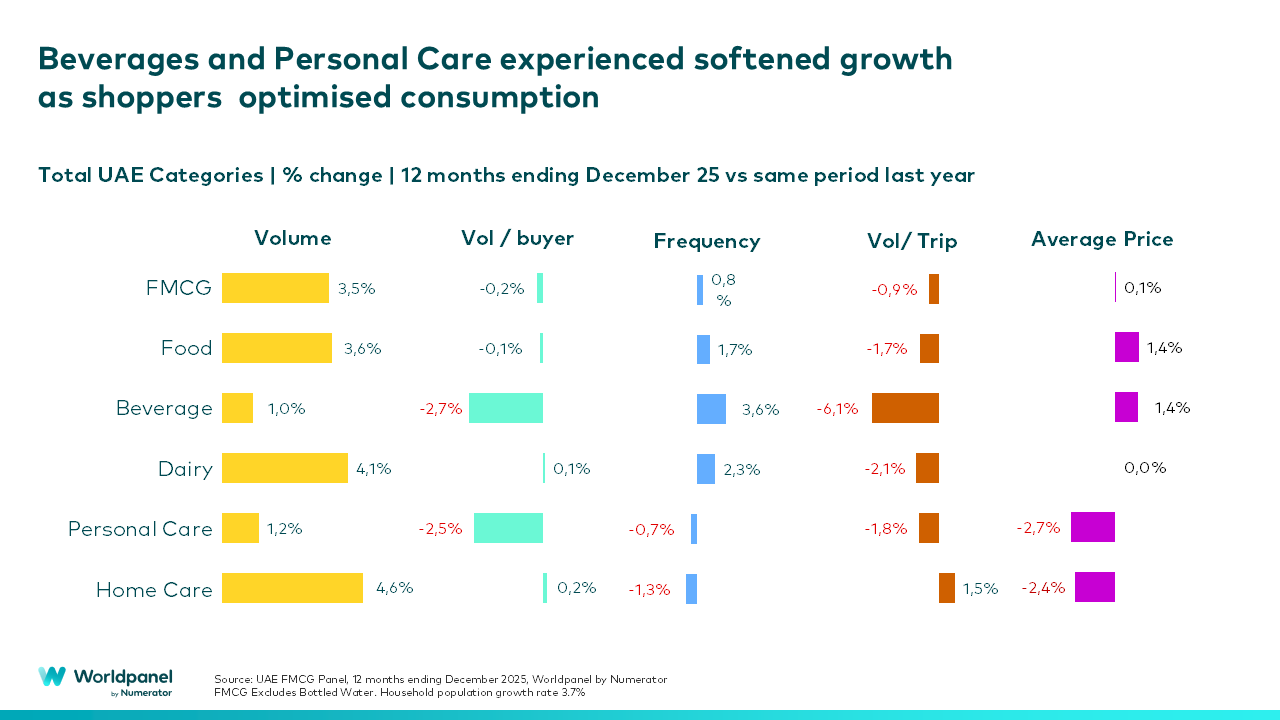

有机产品的消费量正在下降,其中饮料和个人护理类产品的降幅最为显著:

- 饮料:消费者倾向于购买小包装产品,购物频率也随之增加,尤其是软饮料和果汁。尽管购买频率有所增加,但单次购物量却在减少。

- 个人护理:在绝大多数子品类中,消费者正转向小包装产品,并减少购物频率,以此在生活成本上升的情况下平衡预算。

渠道动态

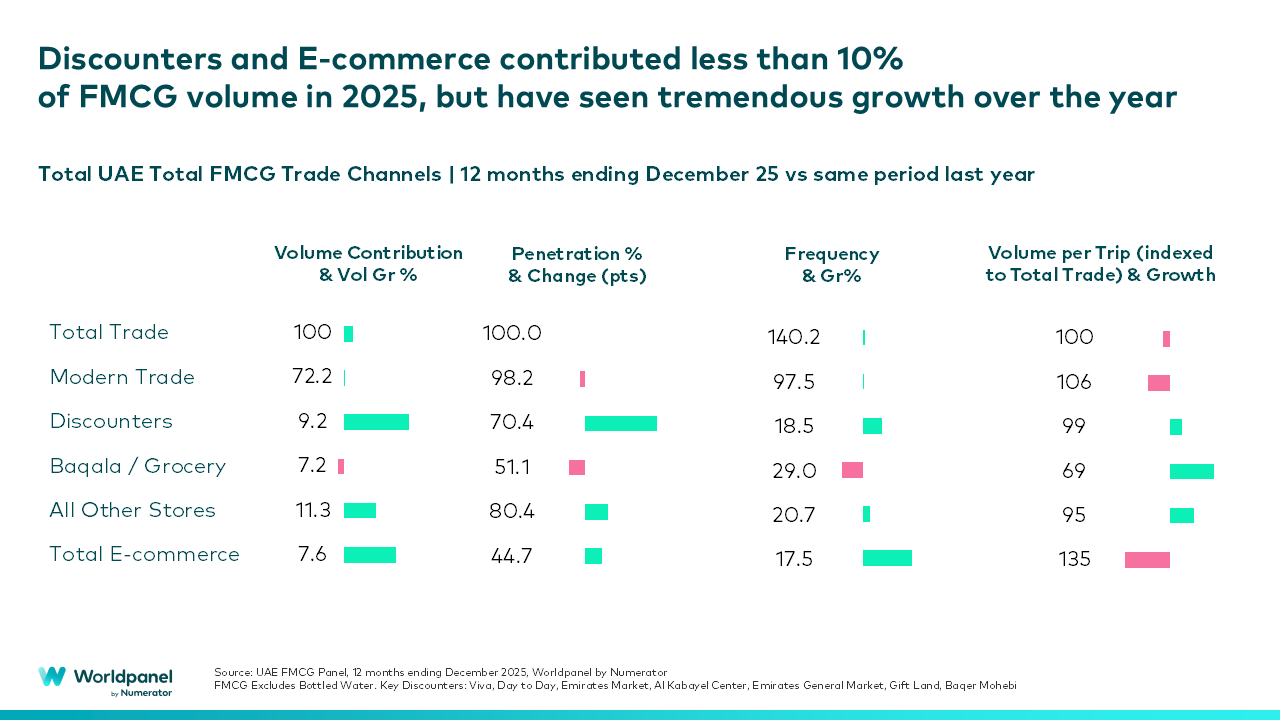

折扣店依然表现突出,通过传达清晰的价值主张实现了快速增长。这些零售商目前占快消品总销量的近10%,显示出对各类消费者群体都极具吸引力。

其增长得益于价格更低、规格更小的中小包装,这与当前消费者的需求高度契合。

这对品牌和零售商意味着什么

阿联酋的快消品市场正在不断发展,最终胜出的将是那些:

- 根据不断变化的消费能力需求调整包装规格

- 围绕“购物频率更高、单次购买金额更小”制定策略

- 在增长势头强劲的渠道——尤其是折扣店——与消费者建立联系

- 针对每位买家消费额下降的品类,重新评估定价和促销策略

若想了解这些变化在不同品类、消费者画像或渠道中的具体表现,我们的专家可为您提供量身定制的洞察分析及战略建议。欢迎随时 联系我们 ,获取免费咨询。

Priyanshu Rana

通过领导力、非洲与中东消费者指数 纽锐拓

.svg)